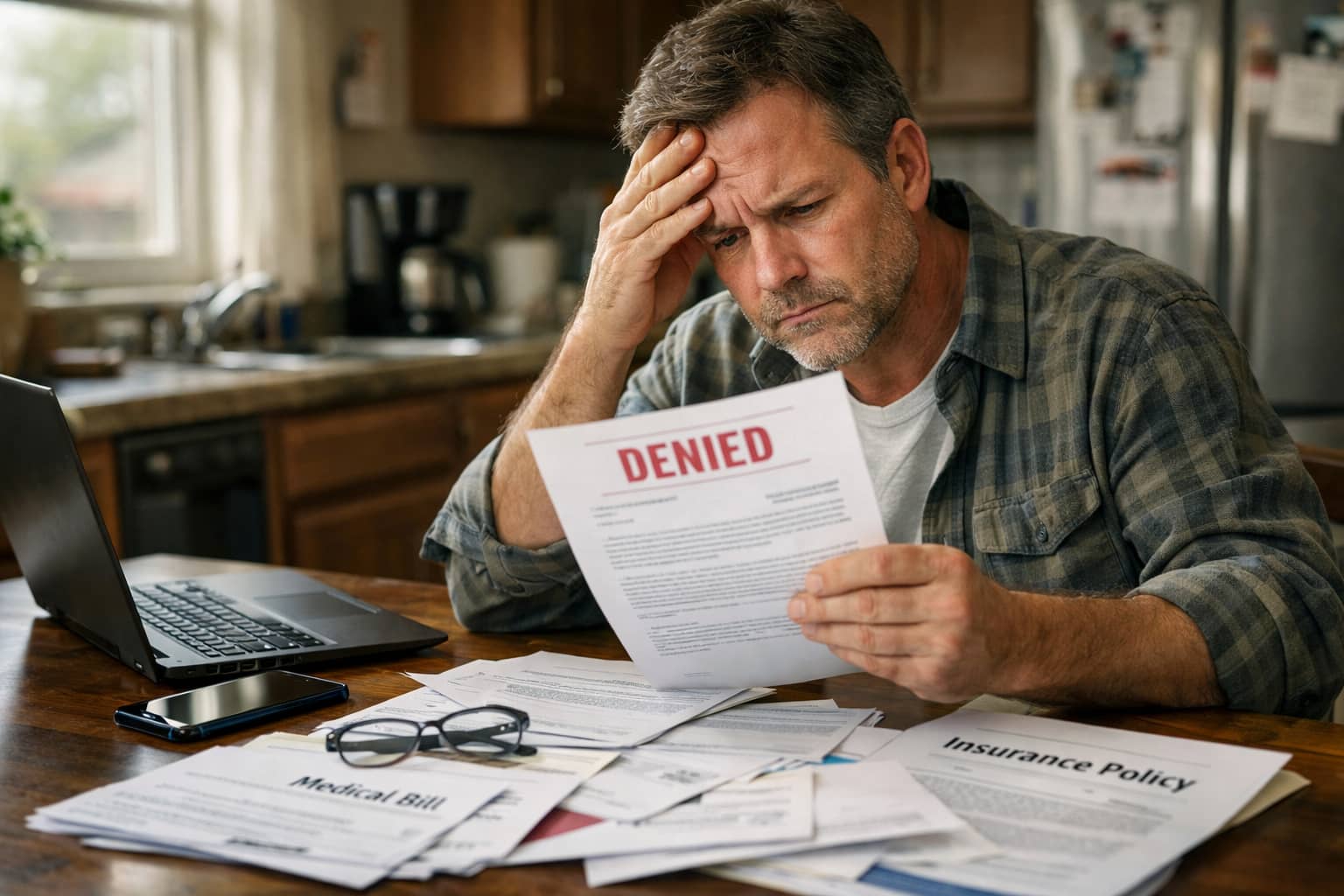

You pay your premiums, answer personal questions, and trust that if a serious illness, disability, property loss, or death occurs, your insurer will honor its side of the bargain.

Then a denial letter arrives. It cites sections of your policy, refers to “insufficient proof,” “non-covered losses,” or “pre-existing conditions,” and leaves you wondering how the safety net you relied on disappeared overnight. The financial consequences are real. So is the feeling that something about the process was not fair.

At Kantor & Kantor LLP, we are people helping people. Our California insurance bad faith attorneys work with individuals and families who find themselves in this position and need a way forward.

Our firm’s role is to help you understand whether your insurer acted within the bounds of California law and the covenant of good faith and fair dealing—or whether the denial crossed the line into bad faith conduct that can be challenged.

If you are staring at a denial letter and unsure what to do next, you do not have to navigate it alone. Call 818-886-2525 or message our bad faith insurance claim denial lawyers online for a free consultation to talk with someone who will listen to your story and help you explore your options.

Contact Kantor & Kantor, LLP online or at 818-886-2525 to begin the conversation.

Why Choose Our Insurance Bad Faith Attorneys in California?

When an insurance company says “no,” it does not just close a claim. It can upend treatment plans, strain family finances, and make every next step feel uncertain. In that kind of moment, you need legal help that understands both the law and what this denial is doing to your life.

Our California insurance bad faith attorneys offer:

- A people-first approach: Your situation is heard and taken seriously, with attention to how the denial is affecting your health, your family, and your stability, not just the numbers on a page.

- Advocacy for policyholders only: The firm stands with individuals and families, not insurance carriers, so the only question is how to protect your rights under the policy.

- Experience with complex denials: The team regularly handles health insurance, disability (including ERISA plans), long-term care, life and accidental death, and homeowners and commercial property claims, bringing practical insight into how and why denials happen.

- An inside view of insurer decision-making: Years of reading claim files, internal notes, and denial letters have shown how insurers investigate, interpret policy language, and sometimes push the limits of California’s bad faith standards.

- Steady guidance through hard decisions:You receive clear, respectful explanations about what the law requires, where your insurer may have fallen short, and what options are realistically on the table, so you are not left trying to piece it together alone.

The goal is to meet you where you are—worried, frustrated, and looking for clarity—and help you move from a confusing denial to a grounded understanding of what can be done next.

What Is Insurance Bad Faith in California?

Insurance bad faith occurs when an insurance company unreasonably denies, delays, or underpays a valid claim, violating its legal duty to act fairly and in good faith toward the policyholder. In California, every insurance contract includes an implied covenant of good faith and fair dealing, which requires insurers to properly investigate claims, evaluate evidence objectively, and honor the coverage promised in the policy.

Bad faith can arise when an insurer prioritizes its financial interests over its obligations to you—such as denying a claim without a thorough investigation, misinterpreting policy language, or failing to respond within required timeframes. When this happens, policyholders may have the right to pursue compensation beyond the original claim, including additional financial losses caused by the insurer’s conduct.

Examples of Insurance Bad Faith Denial Practices in California

Bad faith is not a single act. It is usually a pattern that emerges when you look closely at how a claim was handled from the first notice of loss to the final denial letter.

Denials Without a Reasonable Investigation

California’s Fair Claims Settlement Practices Regulations require insurers to investigate claims thoroughly and in good faith. A denial is suspect when it comes after a limited or one-sided review.

You may see this when:

- A disability claim is denied based only on an internal nurse reviewer’s note, without contacting your treating doctors or obtaining current medical records.

- Long-term care benefits are refused after a cursory assessment, even though more recent evaluations document significant limitations in activities of daily living.

- A health insurance claim for a treatment recommended by your specialist is denied based on generic utilization review guidelines that do not reflect current standards of care.

- A property claim after a fire or leak is denied following a brief inspection that does not include testing for hidden structural or mold damage.

An insurance bad faith attorney can obtain the full claim file, including internal notes, emails, and guidelines, to see what the company actually did before it decided to deny your claim—and what it chose not to do.

Misusing Exclusions and Limitations to Avoid Payment

Every insurance policy contains exclusions and limitations. These terms define what is not covered. Problems arise when insurers stretch these provisions beyond their reasonable meaning.

Some patterns that raise concern include:

- Calling a sudden water leak “long-term seepage” to avoid paying a homeowners claim.

- Labeling a recommended medical treatment as “experimental” when peer-reviewed studies and accepted guidelines support its use.

- Applying a pre-existing condition exclusion to deny a disability or health claim even when the condition did not cause, or only indirectly relates to, the current claim.

- Treating a mental health condition as outside coverage despite parity requirements or policy endorsements.

California law expects insurers to interpret policy language reasonably and in line with the insured’s expectations when purchasing coverage, not in a way that defeats the policy’s central purpose.

Rescission of Coverage After a Loss

In some California cases, the insurer responds to a claim by attempting to void the policy entirely. The company may allege that the application was completed inaccurately, that health information was omitted, or that income or occupation details were misstated.

Rescission is particularly troubling when:

- The inconsistencies involve minor details that had no bearing on the risk insured.

- The insurer had access to the same information, through authorizations or records, at the time of underwriting but did not investigate until after a large claim was filed.

- Premiums were paid for years without objection, only to have the policy declared void once benefits were sought.

Lawyers can compare the alleged misstatements with the insurer’s underwriting guidelines and assess whether rescission is being used fairly—or as a post-claim tool to avoid paying benefits.

Ignoring Evidence That Supports Coverage

Another common thread in potential bad faith cases is selective reading of the evidence. Instead of weighing all relevant information, the insurer may:

- Highlight a single phrase from a medical record while ignoring the overall diagnosis and functional restrictions.

- Emphasize a surveillance clip that shows a brief moment of activity, while disregarding lengthy periods of rest or pain documented in the same timeframe.

- Rely on a single “independent” medical examination that contradicts years of treatment records, without explaining why that one opinion should control the narrative of your payout.

- Discount contractor or engineering reports that document the full scope of property damage.

The covenant of good faith and fair dealing requires insurers to consider the whole picture. When a denial letter reads like it was written with blinders on, it may be time to ask why.

Delay Used as a Path to Denial

California regulations require insurers to acknowledge claims and respond to communications within specific timeframes. Delay becomes a concern when it is part of a trajectory leading toward denial, such as:

- Repeated requests for the same documents, even after you have provided them.

- Shifting explanations about what information is needed to move forward.

- Silence for extended periods, followed by a denial that cites “incomplete documentation” or “failure to provide requested information.”

Delays that ultimately set up a denial can be evidence that the insurer is not engaging with your claim in good faith.

Contact Kantor & Kantor, LLP online or at 818-886-2525 to begin the conversation.

What Damages Can You Recover in an Insurance Bad Faith Claim?

If an insurance company acts in bad faith in California, you may be entitled to recover more than just the benefits originally owed under your policy. Depending on the circumstances, damages can include:

- Policy benefits: The full amount the insurer should have paid on your claim

- Consequential damages: Financial losses caused by the denial, such as medical bills, lost income, or property-related expenses

- Emotional distress: Compensation for stress, anxiety, or hardship resulting from the insurer’s conduct

- Attorney’s fees and costs: In some cases, the cost of pursuing your claim

- Punitive damages: Additional damages meant to punish especially harmful or reckless behavior and deter similar conduct

The exact damages available depend on how the insurer handled your claim and the impact the denial had on your life.

Types of Insurance Bad Faith Cases We Handle in California

Contact our California bad faith insurance claim denial attorneys for a free consultation to discuss how we can help with cases involving:

- ERISA claims: Challenging denials of benefits governed by ERISA, including employer-sponsored disability, life, and other group insurance plans, and guiding you through the strict and technical appeal process so you are not left trying to navigate it alone.

- Insurance bad faith:Examining how your claim was handled, identifying when an insurer’s denial crosses the line into unreasonable or unlawful conduct, and standing up for you when the company does not live up to the promises written into your policy.

- Long-term disability:Pushing back when long-term disability benefits are denied or cut off based on disputed medical opinions, surveillance, or narrow readings of your job duties, and working with you to present the full picture of how your condition affects your daily life.

- Short-term disability:Contesting quick denials or abrupt terminations of short-term disability benefits and helping you assert your right to recover before being pressured to return to work too soon.

- Life insurance:Disputing life insurance denials based on alleged misrepresentations, exclusions, or claimed lapses in coverage, and helping your family pursue the benefits you counted on during an already painful time.

- Long-term care insurance:Advocating for long-term care benefits when an insurer refuses to recognize the level of assistance you or a loved one needs in assisted living, nursing home, memory care, or at home.

- Retirement benefits:Addressing denials or reductions of pensions and other retirement benefits when plan administrators or insurers interpret plan terms in ways that strip away the security you worked for over many years.

- Homeowner’s insurance:Challenging claim denials after fires, water damage, storms, or other losses to your home or belongings, and working to hold your insurer to the coverage you paid for to help you rebuild.

If an insurance company has denied a claim that you or your family were relying on, you do not have to take that as the final answer. During a free case review we can talk about what happened, what your rights are, and how we may be able to help you move forward.

How Kantor & Kantor LLP Helps After a Bad Faith Insurance Claim Denial in CA

Facing a denial from a large insurance company can feel overwhelming. You may be unsure whether to appeal, file a lawsuit, or walk away. Kantor & Kantor LLP steps in to shoulder the legal weight so that you can focus on your health, your family, and your life.

Our insurance bad faith attorneys in California:

- Review your policy and denial letterto identify the provisions the insurer is relying on and how they may relate to California Insurance Code and claims regulations.

- Help obtain the full claim file, including internal notes, evaluation tools, and communication logs, to understand how the decision was made.

- Work with your doctors and other experts to clarify medical issues, functional limitations, or damage assessments that the insurer may have overlooked or downplayed.

- Map the insurer’s conduct against legal standards, including the covenant of good faith and fair dealing and unfair claims settlement practices rules, to determine whether there is a basis for a bad faith claim.

- Pursue appropriate remedies, which may include payment of benefits, compensation for additional losses caused by the denial, and, in some cases, punitive damages where the law allows.

Throughout the process, Kantor & Kantor keeps clients informed and involved, explaining options and likely outcomes so that decisions are made with clarity rather than pressure.

California Insurance Bad Faith Lawyers FAQ

Does a denial letter that mentions “genuine dispute” mean I cannot bring a bad-faith case?

Not necessarily. California’s genuine dispute doctrine protects insurers when there is a reasonable disagreement over coverage, damages, or law. However, the label “genuine dispute” in a letter does not control. Courts look at whether the investigation, evaluation, and decision-making process were reasonable. A lawyer can help assess whether the doctrine truly applies to your situation.

Can I pursue a claim for insurance bad faith if my claim was only partially denied or underpaid?

Yes, in some circumstances. Bad faith can involve partial denials or underpayments if the insurer unreasonably refused to pay the full benefits owed. The key question is whether the amount paid reflects a fair and reasonable evaluation under the policy and California law.

What if ERISA governs my policy—can there still be bad faith remedies?

ERISA-governed employer plans follow different rules than individual policies. While traditional state-law bad faith remedies may be limited for some ERISA claims, there can still be legal consequences for improper handling, and a careful approach to the administrative appeal is critical. An attorney familiar with both ERISA and California insurance law can explain what remedies may be available in your case.

Will bringing a bad faith claim affect my ability to obtain insurance in the future?

Insurers must follow specific rules regarding underwriting, renewal, and cancellation. Exercising your legal rights should not be used as a basis for improper retaliation. If you are concerned about how a dispute might affect future coverage, a lawyer can address those concerns and help you understand the protections that exist.

Talk With Kantor & Kantor LLP About an Insurance Bad Faith Denial in California

When a denial letter arrives, it can feel like the decision has already been made, and there is nothing more you can do. It can also be the moment when you start to question whether your insurance company truly honored the duties of good faith and fair dealing that come with your policy.

Sorting that out on your own—while dealing with medical needs, disability, long-term care decisions, repairs to your home, or the loss of a loved one—can be overwhelming. You deserve clear, direct information about what happened with your claim and what options you may still have.

If your claim for ERISA benefits, long-term disability, short-term disability, long-term care, health, life, homeowner’s, retirement, or other coverage has been denied in California, you do not have to accept that decision without answers.

Call 818-886-2525 or contact Kantor & Kantor LLP online to schedule a free consultation with our California insurance bad faith attorneys and talk about how we may be able to help.

Contact Kantor & Kantor, LLP online or at 818-886-2525 to begin the conversation.

Attorney Glenn R. Kantor

Glenn Kantor is a founding partner of Kantor & Kantor LLP. As a young attorney, Glenn saw the injustice of wrongful insurance denials and created a law firm to represent individuals seeking to obtain their rightful benefits. Glenn is committed to ensure that clients receive the benefits they are entitled to under their insurance policies or group health plans. [Attorney Bio]